The European fertilizer industry is currently navigating its most significant transformation since the Industrial Revolution. Driven by the European Green Deal and the Carbon Border Adjustment Mechanism (CBAM), the sector has shifted from a reliance on imported natural gas to a leadership position in fossil-free nitrogen and circular nutrient recovery.

Key Industry Drivers

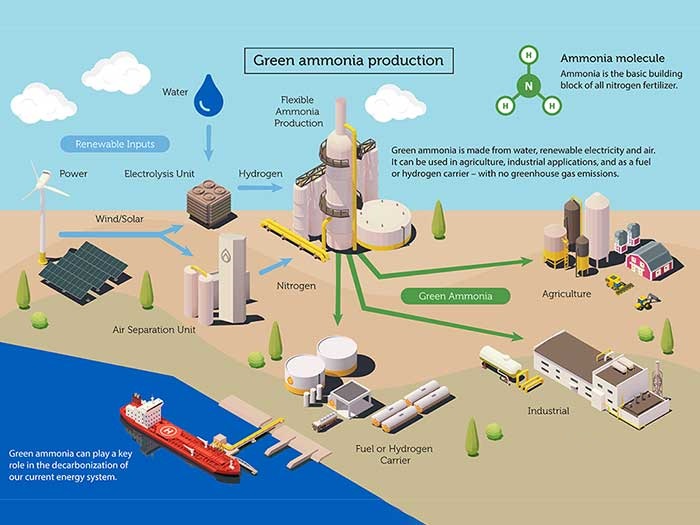

Decarbonization & Green Ammonia

Europe is the global laboratory for Green Ammonia (NH3 produced via water electrolysis using renewable energy).

- Yara and Fertiberia have inaugurated industrial-scale green hydrogen plants, reducing the carbon footprint of NPK fertilizers by up to 90%.

- Policy Impact: The full implementation of CBAM in 2026 has placed high tariffs on carbon-intensive fertilizer imports, making domestic “Green Fertilizer” price-competitive.

Circular Economy & Nutrient Recycling

To reduce dependency on imported phosphate rock (often sourced from North Africa or Russia), Europe has pivoted to Urban Mining.

- Phosphorus Recovery: Countries like Sweden and Germany now mandate the recovery of phosphorus from municipal sewage sludge ash.

- Organic-Mineral Blends: There is a growing market for “Organo-mineral” fertilizers, combining recycled organic waste with precise doses of chemical nutrients.

Current Challenges

- Energy Costs: Despite the rise of renewables, electricity prices in Europe remain volatile, challenging the margins of green hydrogen production compared to cheap US-based natural gas.

- Capital Flight: Some manufacturers have moved high-volume urea production to the US or North Africa (e.g., Egypt) where gas is cheaper, keeping only specialty “Green” production in Europe.

- Technological Risks: As seen with the recent bankruptcy of Cinis Fertilizer in early 2026, scaling green-tech startups remains high-risk despite strong market demand.

Technological Trends in 2026

- Precision Farming Integration: Equipment now includes “Digital Twin” sensors that communicate with fertilizer spreaders for variable-rate application (VRA).

- Controlled-Release Fertilizers (CRF): New EU regulations on microplastics have forced a shift toward biodegradable polymer coatings for slow-release granules.

- Decentralized Production: Growth in “Containerized” nitrogen production units that allow local cooperatives to produce fertilizer using on-site wind or solar power.

Conclusion

The European fertilizer market is no longer a volume-driven commodity market; it is a technology-driven specialty market.